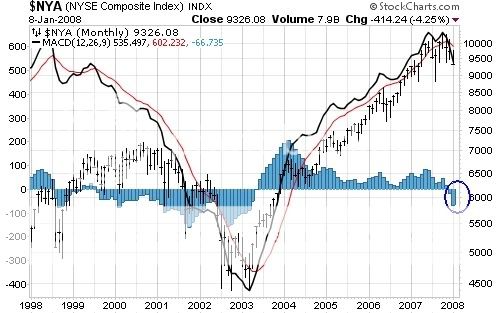

Get out. Everybody get out!

In the beginner's mind there are many possibilities, in the expert's mind there are few.

Get out. Everybody get out!

Golden Oldie

FORBES

Bernard Condon, 12.10.01

Having called the top of the gold market 22 years ago, a goldbug now thinks that he has found the bottom.

In 1977 James Sinclair boldly predicted that gold would rise from $150 per troy ounce to $900. Gold never reached that mark, but it came close on Jan. 21, 1980, peaking at $887.50. The next day, says Sinclair, he unloaded his entire gold position, personally netting $15 million. Pointing to the U.S. Federal Reserve’s efforts to fight inflation, Sinclair then predicted at an annual gold conference that the metal would languish for the next 15 years. It did. On Friday, Jan. 20, 1995, it closed at $383.85.

So this is a guy to listen to. He’s bullish again. Why? Because he believes, despite the whiff of deflation in the October producer price index, that the U.S. is headed for mild inflation. He thinks that the dollar is due for a fall. He is also impressed that mining companies, which routinely sell unmined metal forward at fixed prices to protect themselves against further price drops, have recently pulled back from placing these hedges, a move that should prompt gold prices to rise. If they do, Sinclair expects a squeeze on gold speculators, who have $36 billion in short positions. Sinclair figures that the shorts will cover their positions soon after gold hits $305, a move that could force the price to $350, even $430.

Persuaded? On the New York Mercantile Exchange you can buy an option to purchase 100 ounces of gold in six months with a strike price set at a slight premium to today’s price. An option exercisable at $300 will cost you $9 an ounce. If gold hits $350 you pocket $4,100 in profits.

Sinclair is not buying just futures and options. Since 1996 he has invested $11 million to develop 5,600 square kilometers of barren land in central Tanzania that he’s convinced hold vast gold deposits. Drilling on the property is still in the early stages, but Barrick Gold is already pulling metal from an adjacent site whose proven and probable reserves have nearly tripled to 10 million ounces in the past two and a half years.

It’s a gamble not many investors would make, but Sinclair has always stood apart from the crowd. On the walls of his office hang six photographs of Shri Sathya Sai Baba, a guru in India whom Sinclair visits several times a year. Sinclair’s love of carrot juice recently turned into a 25-kilo-a-week habit that was brought to a halt only when his doctor grew alarmed at the orange tint to his skin. A loner, Sinclair paid $3 million in 1983 to turn a 19th-century barn into a reception hall for his house but has held only three parties there.

After his 1970s career as a goldbug, Sinclair retreated to his Connecticut estate, where he played with his helicopters, show ponies and collection of Ferraris. He didn’t stay idle long. He built cable systems at Cross Country Cable, a company he started with two friends, then made millions selling some of them to John Malone’s TCI.

“Jimmy is different,” says his onetime cable partner Vincent Tese, the former New York State banking commissioner and now a Bear Stearns director. “But in the trading business people don’t care if you’re purple, just as long as you’re making money.”

In 1989 Sinclair got back into metals after buying a small stake in a Vancouver, Canada, mining company called Sutton Resources. During a trip to Tanzania for the company that year to check out a potential nickel site, Sinclair became intrigued by a 140-square-kilometer patch of land called Bulyanhulu. It was studded with greenstones, volcanic rocks marked by long seams that are often rich in minerals. Some greenstone mines, such as those in Canada’s Kirkland Lake Camp, have been yielding gold for a century and do so now at the relatively low cost of $200 an ounce.

“The opportunity stared at me as it did with cable and gold,” he says. “The only way to make big money is to have the courage to put your eggs in one basket.”

Sinclair helped Sutton buy rights to mine Bulyanhulu, then lobbied for it to do the same in adjacent lands. Sutton balked and eventually sold Bulyanhulu to Barrick. Sinclair decided to go it alone.

By the summer of 1999 he had invested $4 million in the lands near Bulyanhulu. He faced a sickening prospect. Gold had just hit a 21-year low of $246. Bears were predicting $150 soon, a price that could wipe out the profits from even the most efficient of Tanzania’s mines.

“I felt a pit in my stomach, like hunger,” Sinclair recalls. “When I was a young trader, I used to think that I was invincible. Now I feel the risk.”

Simple logic mitigated his fears. It costs most companies $250 (including back-office support) to extract an ounce of gold. With gold trading below cost, it made no sense for mining companies to hedge against further price reductions. Recognizing that such hedges meant that an important force pulling gold down would soon disappear, he reasoned that the bottom was near.

Over the next nine months Sinclair spent $1.5 million on tests that measured magnetic pull to help locate seams in his greenstone. Soon after the tests ended, in February 2000, news broke that some big mining companies had indeed stopped placing new hedges. Sinclair reached into his pocket for $5 million to buy more mining rights in surrounding lands. Barrick expects that the $199 an ounce it is paying to mine gold at Bulyanhulu will drop to $130 over the next three years.

Sinclair hopes to sell his operation to a big mining company soon. To do that he’ll need to prove that his gold can be as richly mined as it is in Bulyanhulu. And pray that bullion doesn’t plummet again.

Sinclair’s bullishness is catching on. One well-regarded bear, Andrew Smith of Mitsui, surprised the markets in September by announcing that he expects the metal to go to $340.

‘Mispricing’ could cost Deutsche Bank over $1m

By Goh Eng Yeow, Markets Correspondent

DEUTSCHE Bank could lose more than $1 million after a bungle that underpriced a keenly-awaited new warrant being sold to Singapore investors.

The bank suspended trading of the warrant – issued on Hong Kong-listed China Railway – from 9am yesterday, and it might ask the Singapore Exchange (SGX) to cancel the mispriced trades.

Traders said, however, that should the SGX decline to do so, Deutsche Bank’s losses could well exceed $1 million.

Deutsche Bank announced yesterday afternoon that trading in the warrant would resume at 9am tomorrow.

The bank’s call warrant on China Railway started trading on Monday last week, two weeks after the stock started trading in Hong Kong. Holders can use one warrant to buy two China Railway shares at HK$9.50 each. The warrant expires in June this year.

One dealer said, based on China Railway’s close of HK$10.74 last Friday, the warrant should now be worth over $1, given its long period before maturity.

UNDERPRICED ISSUE

The new warrant was issued by Deutsche Bank at 78.7 cents apiece. It closed last Friday at 77 cents on a heavy volume of 10.65 million shares, after it gained 44.5 cents from Thursday’s close of 32.5 cents.

Deutsche Bank said trading in the warrant was suspended pending the resolution of error trades – ‘due to significant mispricing on its part in the warrant’.

Dealers contacted by The Straits Times believed the warrant attracted heavy trading last Friday, as traders became aware of the serious mispricing. ‘Deutsche Bank will be making a big loss if the bulk of the 10 million warrants was sold by the bank,’ said a remisier.

Still, many were amazed that errors in pricing the warrant went undetected for two days.

‘When Deutsche Bank announced that it was launching the new warrant, it clearly stated that the issue price was 78.7 cents,’ said a market observer.

Warning bells should have been sounded when the warrant was trading at only 32.5 cents last Thursday, even though China Railway’s share price was surging at the time, he added.

Given the two currencies involved, the error could have been caused by a Deutsche Bank trader entering the wrong conversion price into a pricing model.

Still, unless the SGX allows Deutsche Bank to cancel the error trades, there is nothing much the bank can do. ‘There is a consultation paper to give the SGX the power to adjust the transacted price of the trade, rather than cancel them outright, but this policy has not been implemented yet,’ a banker said.

Some traders are also wondering if it is advisable for a warrant issuer to suspend trading of a warrant simply because of error trades.

Deutsche Bank’s warrant mispricing follows error trades at other warrant issuers.

Societe Generale apparently had to pay millions three years ago when a wrong keystroke sent shares of and warrants on Total Access Communications into a tailspin. Last year, DMG & Partners stopped online warrants trades completely, after an Internet trader nearly lost $426,000 on a warrant sale.

You see? Temasek, you see?

Merrill Lynch seeking new capital from Chinese and Mideast investors – report

December 30, 2007: 08:46 AM EST

LONDON, Dec. 30, 2007 (Thomson Financial delivered by Newstex) — The new chief executive of Merrill Lynch (NYSE:MER) (OOTC:MERIZ) & Co Inc is in talks with Chinese and Middle Eastern investors this weekend that could lead to a capital-raising sale of another big stake in the US investment bank, the Observer reported.

John Thain is taking calls from a number of potential buyers, understood to include sovereign wealth funds from the Gulf and China, in a bid to raise extra capital, the newspaper quoted an unidentified US observer as saying.

Singapore state-linked investment company Temasek Holdings (Pte) Ltd said on Dec 26 it had invested 4.4 bln usd into Merrill — equivalent to 91.7 mln of Merrill’s shares at 48 usd a share — plus options to buy more shares worth up to 600 mln usd, as a vote of confidence in Thain’s leadership.

The newspaper quoted the unnamed US observer as saying the Temasek cash would not be enough to insulate the group from the impact of the global credit crunch and another unidentified source as saying Thain was seeking extra overseas capital to boost Merrill’s balance sheet and to avert potential future liquidity problems.

Citi, HSBC among banks considering sale of units

They turn to asset sales to generate immediate cash as credit woes persist

NEW YORK – UNITED States and European banks including Citigroup and HSBC Holdings are mulling over sales of parts of their businesses in a nod to crunch times ahead, the Wall Street Journal reported on its website.

While Citigroup may shed or shut several of its mid-size units, HSBC could exit all or parts of its US$13 billion (S$18.9 billion) auto finance arm, said the paper yesterday, citing unnamed sources.

They estimate that Citigroup could dispose of as much as US$12 billion worth of what are considered non-critical assets. These include Student Loan Corporation; its North American auto lending business; its 24 per cent stake in Brazilian credit card company Redecard; and its Japanese consumer finance business.

Talk of the potential moves comes days after Merrill Lynch announced that it would sell most of its commercial-lending business to General Electric for US$1.3 billion. Morgan Stanley pocketed more than US$250 million last month by selling a slice of its

MSCI investment-analysis unit in a public offering.

‘I think we are going to see a real wave of these coming through in the first half of next year,’ said Morgan Stanley banking analyst Huw van Steenis.

Buyers could be hard to find in an environment where many financial companies are in trouble but analysts said the motivation to sell is strong, said the Journal.

This is because asset sales generate quick cash at a time when banks are likely to face persistent difficulties in borrowing money.

Rates at which banks lend to one another are still prohibitively high because of lingering worries about further losses from US sub- prime mortgage investments, it added. Other sources of funds, such as commercial paper, remain frozen or too expensive.

Several of the world’s largest banks have recently sold multibillion-dollar stakes to state-owned Asian and Middle Eastern investors to boost their capital.

But as banks increasingly take onto their balance sheets assets that had been held off-balance, their capital needs have grown.

In a report this month, Goldman Sachs estimated that US$475 billion of extra assets had been moved to bank balance sheets since the credit crunch sped up earlier this year, said the Journal.

Changes in leadership at Citigroup and HSBC also increased the likelihood of sales, it added. Citigroup recently installed Mr Vikram Pandit as its new chief executive, while Mr Brendan McDonagh took over in February as head of HSBC’s US consumer unit, HSBC Finance Corp, after the unit suffered heavy losses on investments in US home loans.

Dear Temasek shareholder

Did you know that, at the current state of play, several investment banks are technically insolvent the moment they disclose their true financial situation? And that the U.S. Federal Reserve, the European Central Bank (ECB) and the Bank for International Settlements (BIS) are trying their best to prevent such a blowup from occurring, including lending unlimited amounts of money to these banks? Are you aware that the international press is clueless or does not wish to write about what is really going on within the investment banks, much less how structured products are priced, valued and traded? Why do you think that no person, entity or government corporation in the U.S., Europe, or the Asia-Pacific (other than yourself) wanted to touch the shares in these investment banks with a ten foot pole?

The Reason

According to banking regulators, there are three kinds of assets in the world:

Level One assets are actively traded. You can know exactly how much they’re worth based simply on their price in the open market. Examples of Level One assets are common stock, bonds and funds.

Level Two assets are not actively traded. But they’re similar enough to actively traded assets to give you a reasonable estimate of their value. Examples of Level Two assets are preference shares, antiques and paintings.

Level Three assets are the most slippery. In addition to having no active market, they’re so unique, there’s no reliable way to estimate their true value. Instead, all that banks and regulators can do is guess. And the only tools they have to support their guesswork are unproven mathematical formulas. Examples of Level Three assets are structured products like credit derivatives, collateralised debt obligations (CDOs) and credit default swaps (CDS).

Here’s the key:

The money panic brewing today is driven largely by this third kind of asset — derivatives of questionable value that were artificially created by Wall Street brokers, officially sanctioned by Washington regulators, and falsely rated by Wall Street rating agencies.

These are the sinking assets that are hitting the big Wall Street firms … panicking investors all across the U.S. and Europe … even threatening some money market funds.

Some of Wall Street’s investment banks have more Level Three Assets than they have capital

Specifically, according to data compiled by the Financial Times:

Merrill Lynch has US$27.2 billion in Level Three assets, the equivalent of 70% of its stockholders’ equity. In other words, for each $1 of its capital, Merrill has 70 cents in assets of questionable and uncertain value.

Goldman Sachs has US$51 billion in Level Three assets, or 130% of its equity.

Bear Stearns has sunk its balance sheet even deeper into the Level Three asset hole, with US$20.2 billion, or 155% of its equity.

Lehman Brothers is in a similar situation — US$34.7 billion, or 160% of its equity. And …

Morgan Stanley tops them all with US$88.2 billion in Level Three assets, or 250% of its capital. That’s an unwieldy $2.50 cents in Level Three assets for each dollar of capital. It implies that, in the absence of new capital infusions, all it would take is a 40% loss — and Morgan Stanley’s capital could be 100% wiped out.

Bottom line: The huge Wall Street write-downs you’ve heard about to date — among the largest in history — could be just the tip of the iceberg.

All told, there are 968 U.S. commercial banks that invest in derivatives. But among them, 963 banks hold a meager 1.5% of all the interest-rate and credit derivatives in America.

In contrast, just five banks hold an amazingly large 98.5% of all the interest-rate and credit derivatives.

That is why no one in the entire world, other than Qatar, Saudi Arabia and Temasek wanted to become shareholders of UBS or Merrill Lynch! Why would international IBs have to turn up, cap in hand, at the doorsteps of little red dot sovereign funds?

Helping to cut through some of the uncertainty, the Office of the Comptroller of the Currency (OCC) evaluates the credit exposure of each U.S. bank holding derivatives. In other words, it asks the question:

Regardless of whether the bet is a win or a loss, what happens if the investor on the other side of the bet doesn’t pay up?

In normal times, such payment defaults are rare. So this is largely a theoretical question. But in a money panic, when markets can go haywire and available cash financing can suddenly dry up, a chain reaction of defaults could make this a very urgent and practical question. The answers, according to OCC data are that overall, including all types of derivatives:

Wachovia has credit exposure that’s equivalent to 89% of its capital. In other words, if all of its counterparties defaulted on their bets with Wachovia, nearly nine-tenths of its capital would be wiped out.

Bank of America is exposed to the tune of 99% of its capital. Assuming no capital infusions, it could be virtually wiped out in an extreme money panic scenario.

And at three banks, the panic would not have to be quite that extreme:

Citibank has 292% of its capital exposed to this kind of credit risk.

JPMorgan Chase has 387% of its capital exposed.

HSBC beats them all with an exposure of 388% of its capital. That means that even if its counterparties defaulted on just 26% of their bets, its capital could be wiped out.

Now, remember what I told you about Level Three assets — that they don’t have a regular place to trade.

Well, we could say something similar about the overwhelming majority of derivatives: They are not traded on regulated exchanges. Rather, they are traded over the counter, based on individually negotiated contracts.

In other words, if there’s a default, the parties have to work through it directly, one on one. Exchange authorities are not going to step in to help manage the crisis for them.

And currently, four of the five U.S. banks I named earlier trade over 90% of their derivatives in this way — outside of regulated exchanges.

At JPMorgan Chase, Bank of America, Citibank and HSBC, the derivatives they trade outside of exchanges represent 94%, 93%, 97% and 97% of their total, respectively. Only Wachovia has a somewhat lesser amount in this category — 77%.

What does this mean?

That the upcoming financial collapse will be the worst of its kind in human history, and will make 1929 “look like a walk in the park”.

Ah, but you say, ML and UBS are fine. They are immune. They are in a different class altogether. You have spoken to their finance departments, their auditors have produced interim reports. No problem at all.

Well, two points:

1. It is not in the interests of the vendor of an asset (and neither is it under any obligation) to inform you that it’s asset is worthless, or even worse, a liability (aka, caveat emptor).

2. If it’s too good to be true, it usually is.

Man in the News: David Viniar

By Ben White in New York

Financial times

Published: December 21 2007 19:41 | Last updated: December 21 2007 19:41

Call up Goldman Sachs and ask to chat with David Viniar, chief financial officer, and this is the first response you will get: “David hates publicity and would probably rather amputate one of his arms than be interviewed.”

Ring up friends and colleagues and the answers will be similar. “I’ll talk to you,” said one former Goldman executive. “But you cannot possibly quote me. David would rather self-immolate” than be the focus of attention.

Yet there is no avoiding the limelight. In a nightmare year for most investment banks, Goldman just set another earnings record. While others tallied ever-bigger mortgage losses, Goldman made an early call to hedge its mortgage exposure and turned a tidy profit in the process. While no one man, woman or child was responsible for Goldman’s golden call (a fact the bank wants no one to forget), Mr Viniar was certainly a central player, along with Lloyd Blankfein, chief executive, and Gary Cohn and Jon Winkelried, co-presidents.

Mr Viniar was the one who convened the now famous meeting on December 14 2006, in which senior members of the mortgage trading desk, the risk department, the controller’s office and others gathered to discuss the US housing market. They decided that it was time to put hedging strategies in place to prepare for a housing downturn given information from the controller’s office and early losses showing up in Goldman’s mortgage book. The call to hedge was a collective one, but as one senior executive put it: “If it hadn’t been for [Mr Viniar], it probably wouldn’t have happened.”

The hedging worked in fits and starts and eventually produced a profit in the third quarter and left Goldman with a net short position against the mortgage market, a fact Mr Viniar took the rare step of acknowledging when the bank announced earnings.

This week, he returned to form and would not say what Goldman’s stance was on the housing market and added it was unlikely he would ever again acknowledge a proprietary Goldman position.

Mr Viniar, 51, is more than a traditional chief financial officer. He is also in charge of Goldman’s massive back office operations, an area referred to within the bank as “the federation”. (The phrase back office is never uttered at Goldman, presumably because it sounds pejorative.) At some banks being in charge of the back office would not be much to brag about. Not so at Goldman, which places enormous value on technical expertise and the power to crunch massive amounts of data.

John Thain, former Goldman president and now Merrill Lynch chief executive, rose to power through the federation after working as a banker. So did Mr Viniar after Mr Thain plucked him out of investment banking in 1992. So by virtue of what he oversees, Mr Viniar, is extraordinarily powerful for a CFO.

“He is the most influential CFO on Wall Street,” says one former Goldman executive who left recently. “That reflects not only his capabilities, which are enormous, but also Goldman’s treating the back office as an equal partner.”

The fact that other banks do not treat the back office in this way may also explain why they ran into so much more trouble with the mortgage crisis.

Like most Goldman executives, Mr Viniar operates almost entirely behind the scenes, save for his conversations with analysts, investors and reporters during earnings season.

Like Mr Blankfein, Mr Viniar was born in the Bronx. He studied economics at Union College in Schenectady, New York, where he played basketball, a sport he follows to this day with informal games near his home in New Jersey that often include other Goldman executives. He donated $3.2m to the college to build a basketball arena that bears his name. The passion and energy he invested in basketball, Mr Viniar insists, helped him get to the top of his career game. He told the student magazine: “I loved the team and my teammates. I was one of the first ones to show up at practice, the last to leave.”

In a rare personal interview three years ago, Mr Viniar told Institutional Investor magazine: “I’m a very slow, very small forward . . . But I can hit the 15ft jump shot.”

Mr Viniar went on to Harvard Business School and joined Goldman in 1980, where he began as a banker in the structured finance department before moving to head the Treasury department in 1992, the year he became a partner. He became co-chief financial officer in 1994 and chief financial officer just before Goldman went public in 1999.

Mr Viniar, who earned more than $30m last year, played a critical role in 1994 when Goldman was losing millions of dollars a day due to bad proprietary trading bets, an experience colleagues say shaped his approach to risk management. “When you go through a war like that it changes you,” said one former Goldman executive who was then in a senior position. “No one had any clue what was going on.”

The experience did not make Mr Viniar risk averse (Goldman is among the biggest risk takers on Wall Street), it just made him more dedicated to consistently monitoring positions and testing for the worst possible scenarios. Mr Viniar is known to say no often to traders who want to take big bets but also to be careful to ensure the bank is taking enough risk to weather downturns in other parts of the business.

He is known as a quiet, self-effacing family man who never missed a basketball game when the youngest of his four children was at high school. “He would always say we are in a marathon, not a sprint, so take vacations, take time with your family,” said someone who worked under Mr Viniar. “He really did the whole work-life balance thing.”

Of course, when he went to basketball games, he would work in the car on the way there and the way back home or to the office.

If there is criticism of Mr Viniar, it is one that also applies to Goldman as a whole and it is that he provides too little information to investors and analysts about how Goldman makes money in its proprietary trading operations, an area of the bank that some refer to as a black box. “They do a horrible job at investor relations. They refuse to take their investors in as partners,” said Dick Bove, analyst at Punk Ziegel in New York. He added that Mr Viniar “is strong-minded and has a clear sense of what he is willing to do and what he is not willing to do. He has some of that Goldman Sachs arrogance about him. But who cares? The job he has done as CFO is impeccable.”

Merrill Lynch to Get $6.2 Billion From Temasek, Davis

By Yalman Onaran and Chia-Peck Wong

Dec. 24 (Bloomberg) — Merrill Lynch & Co., reeling from the biggest loss in its 93-year history, will receive a cash infusion of as much as $6.2 billion from Singapore’s Temasek Holdings Pte. and Davis Selected Advisors LP.

Temasek will invest up to $5 billion for a less-than 10 percent stake and New York-based money manager Davis Advisors will buy $1.2 billion of Merrill stock, the world’s largest brokerage firm said in a statement today. Merrill fell 2.9 percent to $53.90 at 1 p.m. in New York Stock Exchange trading, after the firm said Temasek will pay $48 a share, almost 14 percent less than the Dec. 21 closing price.

Merrill Chief Executive Officer John Thain, who took over Dec. 1, joins Citigroup Inc., Morgan Stanley and UBS AG in tapping a sovereign wealth fund to shore up capital. An $8.4 billion writedown of mortgage investments and loans led the firm to post a $2.2 billion third-quarter loss and oust CEO Stan O’Neal in October. Merrill may report another $8.6 billion writedown next month, said David Trone, an analyst at Fox-Pitt Kelton Cochrane Caronia Waller.

“Capital raising is a positive” for Merrill, said Mark Batty, who helps manage about $77 billion including Merrill shares at PNC Wealth Management in Philadelphia. “Given the challenge of the hits they’ve received to the equity base, that’s a necessity.”

Merrill also agreed earlier today to sell its commercial finance business to General Electric Co.’s finance arm for an undisclosed price to free up $1.3 billion of capital.

Selling at the Low

Temasek will pay $4.4 billion for new Merrill shares at $48 apiece and has an option to buy an additional $600 million of stock by March 28, according to a term sheet posted on Merrill’s Web site. Davis Advisors, a closely held firm founded in 1969, will make a “long-term investment” of $1.2 billion, according to today’s statement. Davis will also pay $48 a share.

“The only negative for these capital infusions is that they’re selling their stock at the lows,” said Ben Wallace, who helps manage $850 million, including shares of Merrill, at Grimes & Co. in Westborough, Massachusetts. “When you need the money most, you have to accept the low price.”

Temasek’s stake won’t exceed 10 percent, Merrill said. Neither the sovereign fund nor Davis Advisors will play a role in Merrill governance, the company said.

“What we like so much about John Thain is that he has a proven track record of creating shareholder value,” said Kenneth Feinberg, who helps oversee more than $100 billion at Davis Advisors, including its Davis Financial Fund, which has declined 4.6 percent this year.

The Right CEO

The firm had a 0.2 percent stake in Merrill at the end of September, according to a filing with the U.S. Securities and Exchange Commission. Merrill is a passive, minority investor in Bloomberg LP, the parent of Bloomberg News.

Thain, a former Goldman Sachs Group Inc. president, joined Merrill from NYSE Euronext, which he helped transform into a publicly traded company in 2006. By the time his departure as CEO was announced last month, NYSE shares had gained 35 percent since their first day of trading, twice as much as the Standard & Poor’s 500 Index in the same period.

Davis Advisors’ preference for financial stocks dates back to 1947, when Shelby Cullom Davis, the grandfather of the firm’s current chairman, invested $100,000 in insurers at the age of 38. By the time he died in 1994, the sum had grown to almost $900 million, according to John Rothchild’s book “The Davis Dynasty,” published in 2001 by John Wiley & Sons.

Temasek’s Homework

“Davis Funds are very credible,” said Ken Crawford, who helps oversee $900 million, including Merrill shares, at Argent Capital Management in St. Louis. “Their involvement signals that they believe the shares offer value and Thain is the right CEO going forward.”

Governments in the Middle East and Asia have agreed to invest more than $25 billion in Wall Street firms since banks began to disclose subprime losses. Merrill’s shares slumped 40 percent in NYSE trading this year, cutting its market value to $47.5 billion.

“Many take the view that the worst is probably over,” said Teng Ngiek Lian, who oversees $3 billion as head of Target Asset Management in Singapore. Merrill has “written down their books to a comfortable level and I’m sure Temasek would have done its homework.”

Set up in 1974 to run state assets, Temasek now manages a portfolio of more than $100 billion that includes controlling stakes in seven of Singapore’s 10 biggest publicly traded companies.

Abu Dhabi, China

It holds 18 percent of London-based Standard Chartered Plc and 28 percent of DBS Group Holdings Ltd., Southeast Asia’s largest bank.

Temasek, owned by Singapore’s finance ministry, has reaped an 18 percent average annual return since its inception. It raised more than $800 million in the past month selling part of its stakes in China Construction Bank Corp. and Bank of China Ltd., the nation’s second- and third-largest lenders.

Citigroup, the biggest U.S. bank by assets, said Nov. 27 that Abu Dhabi would invest $7.5 billion in the New York-based company. State-controlled China Investment Corp. is buying almost 10 percent of Morgan Stanley for $5 billion after the second-biggest U.S. securities firm reported a loss of $9.4 billion from mortgage-related holdings on Dec. 19.

Government of Singapore Investment Corp., along with an unidentified Middle Eastern investor, agreed this month to inject 13 billion Swiss francs ($11.2 billion) into UBS, the biggest Swiss bank. The government fund manager, known as GIC, manages more than $100 billion of the nation’s foreign reserves.

Bear Trigger

“The valuation for banks seems very reasonable, which is why the sovereign wealth funds are keen,” Target Asset’s Teng said. “We, too, are more bullish about banks generally.”

Investments by sovereign funds may give some respite to banking stocks battered by at least $96 billion of credit- related related writedowns at the world’s biggest financial institutions.

“It just shores up confidence and will boost banking shares,” said Nicholas Yeo, who helps oversee more than $40 billion in Asian equities at Aberdeen Asset Management in Hong Kong. “Maybe the outlook is not so bad.”

Bear Stearns Cos., the securities firm that helped trigger the collapse of the subprime market, struck an agreement in October with China’s government-controlled Citic Securities Co. for a $1 billion cross-investment. The New York-based company announced a $1.9 billion writedown on mortgage losses Dec. 20, sending the firm to its first quarterly loss since it went public in 1985.

GE Capital

General Electric, based in Fairfield, Connecticut, said today it agreed to acquire about $10 billion of assets and $5 billion of commitments from Merrill Lynch Capital, the firm’s commercial finance business.

GE will buy Merrill units that specialize in equipment, franchise, energy and healthcare financing, according to the companies’ statement. The sale, for an undisclosed price, doesn’t include Merrill Capital’s real estate assets.

GE’s finance units, known collectively as GE Capital, have more than $612 billion in assets, with about $260 billion at its commercial finance division.

By now everyone can recite how crummy mortgages got packaged into asset-backed securities, and how, after the tastier tranches were sliced off, the meat by-products got sent along to the CDO sausage factory to be made palatable again. Now CDO investors are puking up all over town.

But there has been another derivatives party going on, where the bubbly is still flowing to a large extent. That, as many will relate, is the explosion in credit default swaps (CDS) that has appeared over just the past few years.

Structured finance has been around since the 1980s, but the CDS market is essentially brand new. The CDS was invented in the mid-1990s but it was minor until the last four years. Since 2003, this market has exploded in size by 10x, to a total notional amount of about $45 trillion. Yes, that’s trillion with a “t”. This market has never been tested in any kind of economic downturn, not even the most recent one of 2001-2002.

The credit-default swap is insurance against a credit accident. The seller of CDS receives a small monthly payment. If the insured bond fails to perform, the buyer of CDS receives a large one-time payment from the seller. At first, in the 1998-2002 period, this was mostly a way for holders of bonds to insure themselves. However, in recent years, the CDS market has become a way for CDS buyers to wager on credit deterioration, and a way for CDS sellers to act like banks.

Banks are a wonderful business, when everything is working right. They have returns on equity that can range from 15% to as much as 25%. These are the kinds of returns that get hedge funds, and their investors, interested. However, it is difficult to enter the banking business. You need offices, branches, depositors, employees, advertising, and so forth.

Banks traditionally profit on the interest rate difference, or “spread”, between the money they borrow, from depositors for example, and the money they lend, to corporations for example. They may lever up ten to one, supporting $100 billion of assets on $10 billion of equity. Thus, if their spread is 2%, and they are levered 10:1, their return on equity is a juicy 20% (actually more like 24% because of the return on the underlying capital).

The CDS contract allowed hedge funds to act like banks. The monthly premium on the CDS is a spread between the equivalent Treasury yield and the implied yield on the underlying bond. This can be considered payment for the risk of default, which the Treasury bond presumably does not have. Imagine you’re a fund with $1 billion in capital. You could try to borrow $9 billion – from whom? – and then buy $10 billion in bonds, and enjoy the spread, like a bank. However, that $9 billion would probably have a higher interest rate than a Treasury bond, because the fund also has risk. And, the maturity of the borrowed money would likely be very short, while the bond has a long maturity, introducing duration risk (this didn’t seem to scare the SIVs however).

The CDS solves these problems. You just sell CDS on $10 billion of bonds. This doesn’t cost any money. You don’t have to put up any collateral. You don’t have to hire a single bank teller or loan officer. You just call your broker, put in the order, and start getting your monthly payments, just as if you had borrowed $9 billion (at the same rate as the Federal government) and lent $10 billion.

And the fund manager who made this one single phone call? If we assume a 20% return, and $1 billion of capital, he collects about $60 million per year. Which explains the explosive growth of the CDS market in the last four years.

Ah, there’s something. You “call your broker.” Actually, you call your dealer. It’s not so easy to just find a buyer for your $10 billion notional of CDS. This is an over-the-counter market. This is where the big broker-dealers, like JP Morgan, Bank of America, and Citibank step in. Over-the-counter markets are lovely for dealers because of the fat spreads – there’s that magic word again that pricks up bankers’ ears – between bid and asked in this market. So, what happens is you sell the CDS to your dealer, such as JP Morgan? JP Morgan then sells CDS – of its own issuance – to its customers that want to buy CDS.

So, you see that JP Morgan now sits in the middle, like a banker should. JP Morgan is “long” the CDS you sold to them, and also “short” the CDS it sold to someone else, and is thus theoretically hedged from risk while collecting the spread between the prices it bought and sold at. This is a lot like bankers’ traditional business of pocketing the spread between the rate it borrows and the rate it lends.

So, it should be no surprise that the big broker/dealer banks (JP, BofA, Citi) account for 40% of the CDS outstanding. Hedge funds account for 32%. This reflects banks’ monkey-in-the-middle dealer strategy for CDS. The remainder is likely insurance companies, synthetic CDOs, CPDOs, and other weird fauna that will soon become extinct. (Thanks go to Ted Seides of ProtÈgÈ Partners for aggregating this information.)

Now, that 32% of CDS sold by hedge funds has a notional value of $14.5 trillion. This means that, if all those bonds underlying the CDS were a total loss, the funds would have to pay $14.5 trillion. Not very likely. However, if there were only a 5% loss – not so impossible these days – the CDS-selling hedge funds would still be on the hook for $725 billion. Hedge funds, all together, have estimated assets of around $2.5 trillion. However, only a small fraction of those are CDS-sellers. Let’s take a guess at 10%, or $250 billion of capital. (It’s probably less than that.) How do you pay a $725 billion bill with $250 billion of capital?

There’s an easy answer to that: you don’t. So, who pays? The banks, remember, are in the middle. If the CDS-selling hedge fund doesn’t pay up on its $725 billion, then the bank is unhedged regarding the CDS that it sold. In this case, the banks would be liable for $475 billion. This is known as counterparty risk.

That’s four-seventy-five billion. More than four times the entire capital of Citigroup – capital which has already come under pressure from losses elsewhere.

So, what happens if there is a CDS counterparty-risk event? Do the big banks go bankrupt? Probably not, although there would be much wailing and gnashing of teeth. Instead, they would probably get a nod and a wink from the government to simply ignore their own CDS obligations. The counterparty risk shifts to CDS-buyers.

The CDS buyers can take the hit, because they aren’t really out any money. They paid their monthly insurance bills, but never got a payout after the credit market car crash. So, in a sense, this drama would likely end in more of a whimper than a bang. In fact, everyone got off OK: the CDS-selling hedge fund manager made a killing in management fees, before the fund went bust; the bank made a killing in dealer income, before kissing their obligations goodbye, and the CDS-buying hedge fund manager raked in the fees on the enormous mark-to-market profits of his CDS portfolio (20% of the aforementioned $725 billion), before these profits were eventually shown to be uncollectible. A perfect Wall Street happy ending.

However, the kind of situation in which large banks ignore multi-hundred billions of legal obligations is very extreme. The last time something like that happened was in the early 1930s. At that time, they called it a “bank holiday,” which has a nice festive ring. The celebration included a devaluation of the dollar, the first permanent devaluation in U.S. history. At least president Roosevelt had the good sense to repeg the dollar to gold at $35/ounce, parity it maintained until 1971. Feel free to make your own guesses as to what Paulson and Bernanke might try.

Regards,

Nathan Lewis

Betting against gold is the same as betting on governments. He who bets on governments and government money bets against 6,000 years of recorded human history.

~Charles De Gaulle~