Category: International Finance

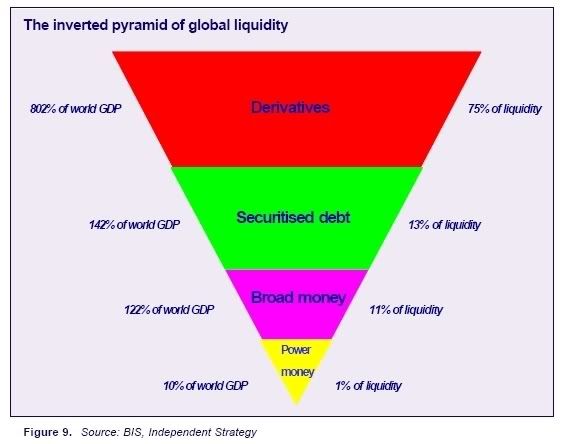

Derivatives

Notional Value

The total value of a leveraged position’s assets. This term is commonly used in the options, futures and currency markets because in them a very little amount of invested money can control a large position (have a large consequence for the trader).

For example, one S&P 500 Index futures contract obligates the buyer to 250 units of the S&P 500 Index. If the index is trading at $1,000, then the single futures contract is similar to investing $250,000 (250 x $1,000). Therefore, $250,000 is the notional value underlying the futures contract.

Credit Derivative

Privately held negotiable bilateral contracts that allow users to manage their exposure to credit risk. Credit derivatives are financial assets like forward contracts, swaps, and options for which the price is driven by the credit risk of economic agents (private investors or governments).

For example, a bank concerned that one of its customers may not be able to repay a loan can protect itself against loss by transferring the credit risk to another party while keeping the loan on its books.

Credit Default Swap

A swap designed to transfer the credit exposure of fixed income products between parties.

The buyer of a credit swap receives credit protection, whereas the seller of the swap guarantees the credit worthiness of the product. By doing this, the risk of default is transferred from the holder of the fixed income security to the seller of the swap.

For example, the buyer of a credit swap will be entitled to the par value of the bond by the seller of the swap, should the bond default in its coupon payments.

Black swan theory

“So far, the losses reported on Wall Street are staggering. But rumors of much larger losses are being whispered…and at least one source has suggested that the firms may be bankrupt…crushed by total system-wide losses of more than $3 trillion.”

In Nassim Taleb’s definition, a “black swan” is a large-impact, hard-to-predict, and rare event beyond the realm of normal expectations. Taleb regards many scientific discoveries as black swans—”undirected” and unpredicted. He gives the September 11, 2001 attacks as an example of a Black Swan event.

The term black swan comes from the ancient Western conception that all swans were white. In that context, a black swan was a metaphor for something that could not exist. The 17th Century discovery of black swans in Australia metamorphosed the term to connote that the perceived impossibility actually came to pass.

Taleb’s Black Swan has a central and unique attribute: the high impact. His claim is that almost all consequential events in history come from the unexpected—while humans convince themselves that these events are explainable in hindsight.

Taleb believes that most people ignore “black swans” because we are more comfortable seeing the world as something structured, ordinary, and comprehensible. Taleb calls this blindness the Platonic fallacy, and argues that it leads to three distortions:

1. Narrative fallacy: creating a story post-hoc so that an event will seem to have a cause.

2. Ludic fallacy: believing that the structured randomness found in games resembles the unstructured randomness found in life. Taleb faults random walk models and other inspirations of modern probability theory for this inadequacy.

3. Statistical regress fallacy: believing that the probability of future events is predictable by examining occurrences of past events.

He also believes that people are subject to the triplet of opacity, through which history is distilled even as current events are incomprehensible. The triplet of opacity consists of

1. an illusion of understanding of current events

2. a retrospective distortion of historical events

3. an overvalue of facts, combined with an overvalue of the intellectual elite

Singapore apparently paid Citi more when China refused

Singapore apparently paid Citi more when China refused

By MarketWatch

Last update: 9:25 a.m. EST Jan. 15, 2008

The Singapore government’s main investment vehicle agreed to increase the amount it planned to inject into Citigroup (C:C 26.24, -0.70, -2.6%) “apparently to cover” the approximately $2 billion Citi had unsuccessfully sought from the government of China, a person familiar with the situation said Tuesday.

During most of the day, Government of Singapore Investment Corp. (GIC) was committed to invest about $4.8 billion to $5 billion in Citigroup, but later in the day apparently told Citi it would “cover” the amount of money ($1.8 billion to $2 billion) the bank had hoped to raise from the Chinese government, the person said.

GIC’s decision partly reflected GIC’s long-standing relationship with the new CEO of Citi, Vikram Pandit, the person said. GIC was an original investor in Old Lane Partners, a hedge fund Pandit co-founded; it was later bought by Citigroup.

China Development Bank’s rejection of Citi’s request emerged Monday night.

The Singapore government would consider additional investments in Citigroup “if the opportunity and the need arises,” the person said.

Singapore has two sovereign wealth funds – GIC and Temasek Holdings Pte. – which have taken stakes in troubled financial institutions in recent months.

The terms of GIC’s purchase of $6.88 billion in Citi convertible bonds reflect the cash-strapped bank’s lack of leverage: GIC said the instruments will earn a hefty 7% non-cumulative interest, payable quarterly.

The conversion premium is a fairly low 20% and is “subject to adjustment in certain limited circumstances.” However, GIC noted these instruments give “appropriate downside protection.”

The press release didn’t give further details.

All told, GIC will own 4% of Citi as a result of the transaction; it already held 0.3% of the bank. GIC said it won’t “take” a board seat at Citi. Indeed, political sensitivities have prompted sovereign wealth funds providing financial infusions to U.S. and European banks to emphasize their intended roles as passive investors.

GIC pumps S$9.8b into Citigroup

GIC pumps S$9.8b into Citigroup

By May Wong, Channel NewsAsia | Posted: 15 January 2008 1951 hrs

SINGAPORE: The Government of Singapore Investment Corporation (GIC) will soon have a bigger stake in US-based Citigroup.

GIC will pump in US$6.88 billion (S$9.8 billion) into one of the world’s largest banks. This is part of Citigroup’s bid to raise US$12.5 billion of capital to boost its financial position.

GIC is the hand behind the management and enhancement of Singapore’s reserves.

That is exactly what the company is doing with its latest purchase into Citigroup. The two companies took just eight days to seal the deal.

GIC’s investment is done through a financial instrument called convertible preferred securities. This will effectively give GIC some form of protection.

For example, if Citigroup’s stock price falls, GIC does not have to convert its securities into shares and will continue to earn dividends of 7 percent.

But such a prudent investment, with lower risks, will also mean that GIC will see relatively lower returns.

In a news release, GIC’s deputy chairman and executive director, Tony Tan, said the company looks for returns on a long-term basis. He believes GIC’s latest Citigroup investment will meet that objective.

Dr Tan said: “GIC is a financial investor seeking commercial returns on a long-term basis … We believe that the investment in Citigroup will meet our long-term investment objective in terms of risk and return.”

GIC now holds 0.3% of shares in Citigroup. The new deal will bring GIC’s stake in the bank to 4% if converted to shares.

The investment will make GIC, as a single entity, one of the top five investors in Citigroup. However, GIC says it will not sit on Citigroup’s board.

GIC’s latest investment comes hot on the heels of a major deal last month, when it pumped nearly S$14 billion into the Swiss banking giant UBS. – CNA/ir

Citigroup, Merrill Lynch Get $21 Billion From Outside Investors

Citigroup, Merrill Lynch Get $21 Billion From Outside Investors

By Yalman Onaran

Jan. 15 (Bloomberg) — Citigroup Inc. and Merrill Lynch & Co., two of America’s largest financial institutions, turned to outside investors for a second time in two months to replenish capital eroded by subprime mortgage losses.

Citigroup, the biggest U.S. bank, is getting $14.5 billion from investors, including the governments of Singapore and Kuwait, former Chairman Sanford Weill, and Saudi Prince Alwaleed bin Talal, the New York-based company said today in a statement. Merrill, the largest brokerage, said it’s receiving $6.6 billion from a group led by Tokyo-based Mizuho Financial Group Inc., the Kuwait Investment Authority and the Korean Investment Corp.

Wall Street banks have now received $59 billion, mostly from investors in the Middle East and Asia, to shore up balance sheets battered by more than $100 billion of writedowns from the declining values of mortgage-related assets. Citigroup was propped up in November by a $7.5 billion investment from the Abu Dhabi Investment Authority. New York-based Merrill was helped by a $5.6 billion cash infusion last month from Singapore’s Temasek Holdings Pte. and U.S. fund manager Davis Selected Advisors LP.

“The only reason the banks are raising capital from the Middle East and Asia is because those are the only people who have the excess capital to lend,” said Jon Fisher, who helps oversee $22 billion at Minneapolis-based Fifth Third Asset Management, which holds shares of Citigroup and Merrill.

Citigroup declined 68 cents to $28.38 and Merrill fell $1.25 to $54.72 in early New York trading.

The writedowns have reduced Citigroup’s so-called Tier 1 capital ratio, which regulators monitor to assess a bank’s ability to withstand loan losses. With today’s capital increase, the Tier 1 ratio would be 8.2 percent, Citigroup said, keeping it above the company’s 7.5 percent target.

`Capital at a Cost’

Morgan Stanley, UBS AG, Merrill Lynch & Co. and Bear Stearns Cos. also reached out to sovereign wealth funds or state- controlled investment authorities in Asia for money after bad investments depressed profits.

“It does show that investors aren’t completely ignoring the sector,” said Peter Plaut, a senior credit analyst at Sanno Point Capital Management, a hedge fund based in New York. “They are putting in capital but it’s at a cost. Now it’s up to the CEOs to be able to generate returns that exceed that cost of capital.”

The Kuwait Investment Authority, which invested in both Merrill and Citigroup, was formed by the Middle East’s fourth- biggest oil producing country in the 1980s to manage the nation’s wealth. Kuwait may have as much as $250 billion of assets, compared with about $875 billion for the Abu Dhabi Investment Authority, the world’s largest sovereign wealth fund, according to an estimate by Morgan Stanley analyst Stephen Jen.

Singapore, Alwaleed

The Government of Singapore Investment Corp. invested almost $7 billion in Citigroup convertible preferred securities and said in a statement today that it will own about 4 percent of the bank if the securities are turned into shares. With a 4 percent stake, Alwaleed has been Citigroup’s biggest individual shareholder since the early 1990s, when soured investments in commercial real estate left corporate predecessor Citicorp short of capital.

Singapore and Alwaleed, along with Los Angeles-based Capital Group Cos., the biggest U.S. manager of stock and bond mutual funds, Kuwait, the New Jersey Division of Investment and Weill, will receive a 7 percent annual dividend from the investment in Citigroup.

Merrill’s convertible securities will pay a 9 percent annual dividend on the securities until they automatically turn into Merrill shares in 2 3/4 years’ time. The group will get fewer shares if Merrill’s stock price climbs above $61.31 and more if it drops below $52.40, according to the company’s statement.

SEC’s Concern

Foreign investors whose stakes rise about 10 percent trigger a review by the U.S. Committee on Foreign Investment, which examines whether acquisitions by overseas buyers compromise national security.

U.S. Securities and Exchange Commission Chairman Christopher Cox said in December that the growth of state-run investment funds may lead to an increase in political corruption because governments might abuse the funds’ leverage over markets and companies.

While there may be “hand-wringing” in Washington over the investments, there won’t be an attempt to tighten rules on foreign investors, said Todd Malan, executive director of the Organization for International Investment.

“Congress realizes that we need this investment,” said Malan, whose Washington-based group represents 141 non-U.S. companies investing in the country.

The following is a table showing banks and securities firms that have sold stakes to shore up capital. All except Barclays Plc raised the cash after reporting asset writedowns and credit losses amid the collapse of the U.S. subprime mortgage market.

Firm Infusion Investor Stake

Citigroup $6.8 Government of Singapore 3.7%

Investment Corp.

7.7 Kuwait Investment Authority; not

Alwaleed bin Talal; Capital specified

Research; Capital World;

Sandy Weill; public investors.

7.5 Abu Dhabi Investment

Authority 4.9%

Merrill Lynch 6.6 Korean Investment Corp.; not

Kuwait Investment Authority; specified

Mizuho Financial Group

4.4* Temasek Holdings 9.4%**

(Singapore)

1.2 Davis Selected Advisors

(U.S.) 2.6%**

UBS 9.7 Government of Singapore

Investment Corp. 10%

1.8 Unidentified Middle Eastern

Investor 2%

Morgan Stanley 5 China Investment Corp. 9.9%

Barclays 3 China Development Bank 3.1%

2 Temasek Holdings 2.1%

Canadian Imperial 2.7 Li Ka-Shing; Manulife not

Financial; others specified

Bear Stearns 1 Citic Securities Co. 6%***

(China)

_____

TOTAL $59.4

* Temasek has an option to invest an additional $600 million.

** Estimate based on purchase price of $48 a share.

*** Citic has an option to increase its stake by as much as

3.3 percent.

Good bankers

Good bankers, like good tea, can only be appreciated when they are in hot water.

– Jafar Hussein, Governer, Malaysian Central Bank

Ten little Injuns

Ten little Injuns standin’ in a line,

One toddled home and then there were nine;

Nine little Injuns swingin’ on a gate,

One tumbled off and then there were eight.

One little, two little, three little, four little, five little Injun boys,

Six little, seven little, eight little, nine little, ten little Injun boys.

Eight little Injuns gayest under heav’n.

One went to sleep and then there were seven;

Seven little Injuns cuttin’ up their tricks,

One broke his neck and then there were six.

Six little Injuns all alive,

One kicked the bucket and then there were five;

Five little Injuns on a cellar door,

One tumbled in and then there were four.

Four little Injuns up on a spree,

One got fuddled and then there were three;

Three little Injuns out on a canoe,

One tumbled overboard and then there were two.

Two little Injuns foolin’ with a gun,

One shot t’other and then there was one;

One little Injun livin’ all alone,

He got married and then there were none.

One little, two little, three little Indians

Four little, five little, six little Indians

Seven little, eight little, nine little Indians

Ten little Indian boys.

Ten little, nine little, eight little Indians

Seven little, six little, five little Indians

Four little, three little, two little Indians

One little Indian boy.

Golden Oldie

Golden Oldie

FORBES

Bernard Condon, 12.10.01

Having called the top of the gold market 22 years ago, a goldbug now thinks that he has found the bottom.

In 1977 James Sinclair boldly predicted that gold would rise from $150 per troy ounce to $900. Gold never reached that mark, but it came close on Jan. 21, 1980, peaking at $887.50. The next day, says Sinclair, he unloaded his entire gold position, personally netting $15 million. Pointing to the U.S. Federal Reserve’s efforts to fight inflation, Sinclair then predicted at an annual gold conference that the metal would languish for the next 15 years. It did. On Friday, Jan. 20, 1995, it closed at $383.85.

So this is a guy to listen to. He’s bullish again. Why? Because he believes, despite the whiff of deflation in the October producer price index, that the U.S. is headed for mild inflation. He thinks that the dollar is due for a fall. He is also impressed that mining companies, which routinely sell unmined metal forward at fixed prices to protect themselves against further price drops, have recently pulled back from placing these hedges, a move that should prompt gold prices to rise. If they do, Sinclair expects a squeeze on gold speculators, who have $36 billion in short positions. Sinclair figures that the shorts will cover their positions soon after gold hits $305, a move that could force the price to $350, even $430.

Persuaded? On the New York Mercantile Exchange you can buy an option to purchase 100 ounces of gold in six months with a strike price set at a slight premium to today’s price. An option exercisable at $300 will cost you $9 an ounce. If gold hits $350 you pocket $4,100 in profits.

Sinclair is not buying just futures and options. Since 1996 he has invested $11 million to develop 5,600 square kilometers of barren land in central Tanzania that he’s convinced hold vast gold deposits. Drilling on the property is still in the early stages, but Barrick Gold is already pulling metal from an adjacent site whose proven and probable reserves have nearly tripled to 10 million ounces in the past two and a half years.

It’s a gamble not many investors would make, but Sinclair has always stood apart from the crowd. On the walls of his office hang six photographs of Shri Sathya Sai Baba, a guru in India whom Sinclair visits several times a year. Sinclair’s love of carrot juice recently turned into a 25-kilo-a-week habit that was brought to a halt only when his doctor grew alarmed at the orange tint to his skin. A loner, Sinclair paid $3 million in 1983 to turn a 19th-century barn into a reception hall for his house but has held only three parties there.

After his 1970s career as a goldbug, Sinclair retreated to his Connecticut estate, where he played with his helicopters, show ponies and collection of Ferraris. He didn’t stay idle long. He built cable systems at Cross Country Cable, a company he started with two friends, then made millions selling some of them to John Malone’s TCI.

“Jimmy is different,” says his onetime cable partner Vincent Tese, the former New York State banking commissioner and now a Bear Stearns director. “But in the trading business people don’t care if you’re purple, just as long as you’re making money.”

In 1989 Sinclair got back into metals after buying a small stake in a Vancouver, Canada, mining company called Sutton Resources. During a trip to Tanzania for the company that year to check out a potential nickel site, Sinclair became intrigued by a 140-square-kilometer patch of land called Bulyanhulu. It was studded with greenstones, volcanic rocks marked by long seams that are often rich in minerals. Some greenstone mines, such as those in Canada’s Kirkland Lake Camp, have been yielding gold for a century and do so now at the relatively low cost of $200 an ounce.

“The opportunity stared at me as it did with cable and gold,” he says. “The only way to make big money is to have the courage to put your eggs in one basket.”

Sinclair helped Sutton buy rights to mine Bulyanhulu, then lobbied for it to do the same in adjacent lands. Sutton balked and eventually sold Bulyanhulu to Barrick. Sinclair decided to go it alone.

By the summer of 1999 he had invested $4 million in the lands near Bulyanhulu. He faced a sickening prospect. Gold had just hit a 21-year low of $246. Bears were predicting $150 soon, a price that could wipe out the profits from even the most efficient of Tanzania’s mines.

“I felt a pit in my stomach, like hunger,” Sinclair recalls. “When I was a young trader, I used to think that I was invincible. Now I feel the risk.”

Simple logic mitigated his fears. It costs most companies $250 (including back-office support) to extract an ounce of gold. With gold trading below cost, it made no sense for mining companies to hedge against further price reductions. Recognizing that such hedges meant that an important force pulling gold down would soon disappear, he reasoned that the bottom was near.

Over the next nine months Sinclair spent $1.5 million on tests that measured magnetic pull to help locate seams in his greenstone. Soon after the tests ended, in February 2000, news broke that some big mining companies had indeed stopped placing new hedges. Sinclair reached into his pocket for $5 million to buy more mining rights in surrounding lands. Barrick expects that the $199 an ounce it is paying to mine gold at Bulyanhulu will drop to $130 over the next three years.

Sinclair hopes to sell his operation to a big mining company soon. To do that he’ll need to prove that his gold can be as richly mined as it is in Bulyanhulu. And pray that bullion doesn’t plummet again.

Sinclair’s bullishness is catching on. One well-regarded bear, Andrew Smith of Mitsui, surprised the markets in September by announcing that he expects the metal to go to $340.

'Mispricing' could cost Deutsche Bank over $1m

‘Mispricing’ could cost Deutsche Bank over $1m

By Goh Eng Yeow, Markets Correspondent

DEUTSCHE Bank could lose more than $1 million after a bungle that underpriced a keenly-awaited new warrant being sold to Singapore investors.

The bank suspended trading of the warrant – issued on Hong Kong-listed China Railway – from 9am yesterday, and it might ask the Singapore Exchange (SGX) to cancel the mispriced trades.

Traders said, however, that should the SGX decline to do so, Deutsche Bank’s losses could well exceed $1 million.

Deutsche Bank announced yesterday afternoon that trading in the warrant would resume at 9am tomorrow.

The bank’s call warrant on China Railway started trading on Monday last week, two weeks after the stock started trading in Hong Kong. Holders can use one warrant to buy two China Railway shares at HK$9.50 each. The warrant expires in June this year.

One dealer said, based on China Railway’s close of HK$10.74 last Friday, the warrant should now be worth over $1, given its long period before maturity.

UNDERPRICED ISSUE

The new warrant was issued by Deutsche Bank at 78.7 cents apiece. It closed last Friday at 77 cents on a heavy volume of 10.65 million shares, after it gained 44.5 cents from Thursday’s close of 32.5 cents.

Deutsche Bank said trading in the warrant was suspended pending the resolution of error trades – ‘due to significant mispricing on its part in the warrant’.

Dealers contacted by The Straits Times believed the warrant attracted heavy trading last Friday, as traders became aware of the serious mispricing. ‘Deutsche Bank will be making a big loss if the bulk of the 10 million warrants was sold by the bank,’ said a remisier.

Still, many were amazed that errors in pricing the warrant went undetected for two days.

‘When Deutsche Bank announced that it was launching the new warrant, it clearly stated that the issue price was 78.7 cents,’ said a market observer.

Warning bells should have been sounded when the warrant was trading at only 32.5 cents last Thursday, even though China Railway’s share price was surging at the time, he added.

Given the two currencies involved, the error could have been caused by a Deutsche Bank trader entering the wrong conversion price into a pricing model.

Still, unless the SGX allows Deutsche Bank to cancel the error trades, there is nothing much the bank can do. ‘There is a consultation paper to give the SGX the power to adjust the transacted price of the trade, rather than cancel them outright, but this policy has not been implemented yet,’ a banker said.

Some traders are also wondering if it is advisable for a warrant issuer to suspend trading of a warrant simply because of error trades.

Deutsche Bank’s warrant mispricing follows error trades at other warrant issuers.

Societe Generale apparently had to pay millions three years ago when a wrong keystroke sent shares of and warrants on Total Access Communications into a tailspin. Last year, DMG & Partners stopped online warrants trades completely, after an Internet trader nearly lost $426,000 on a warrant sale.